1. Definition and Curve Dynamics

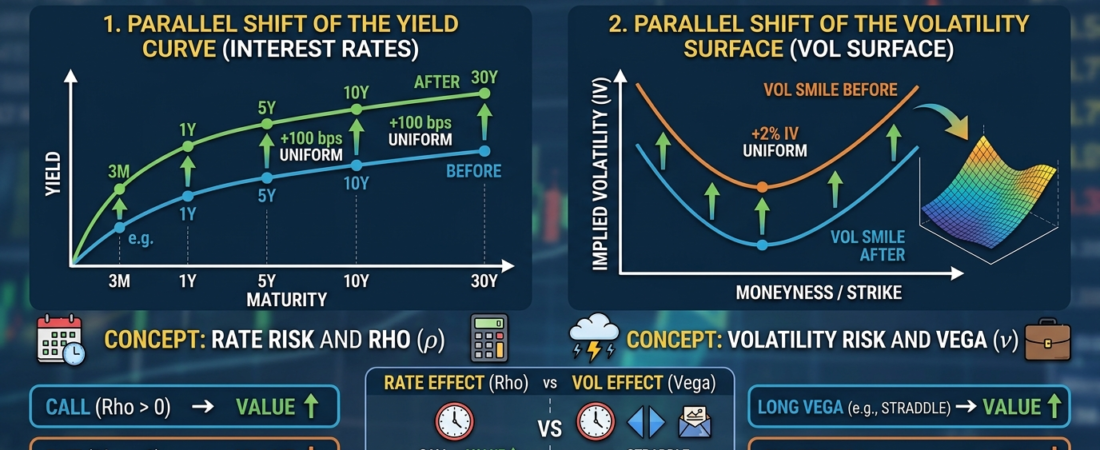

A Parallel Shift represents a rigid and uniform translation of the Yield Curve (or the Volatility Surface). Mathematically, for any given maturity $T$, the new parameter is defined as:

$$r_{\text{new}}(T) = r_{\text{old}}(T) + \Delta$$

Where $\Delta$ is a constant expressed in basis points (bps). In this configuration, term spreads (slope) and curvature remain constant; the curve undergoes a vertical translation exclusively along the y-axis.

2. Impact on Pricing and Discount Factors

In options modeling, a parallel shift in rates affects two primary pricing pillars:

- Discounting: It alters the Present Value (PV) of future payoffs via the discount factor $e^{-rT}$. A positive shift (increase in rates) reduces the present value of option premiums.

- Forward Estimation: For Interest Rate (IR) options (such as Caps, Floors, and Swaptions) or Equity options, it modifies forward rates and the forward price of the underlying asset.

- Equity Calls: Generally exhibit a positive correlation with rates (positive Rho), as the increase in the underlying’s cost of carry typically offsets the discounting of the payoff.

- Interest Rate Options (IR): A parallel shift has an exponential impact, as it simultaneously recalibrates all forward rates that determine the option’s moneyness at exercise.

3. Sensitivity Analysis (Greeks)

Monitoring this phenomenon is conducted through specific risk metrics:

| Shift Scope | Reference Greek | Technical Description |

| Yield Curve | Rho ($\rho$) | Measures the first-order derivative of the option price with respect to a parallel change in the interest rate $r$. |

| Vol Surface | Parallel Vega | Represents the portfolio’s sensitivity to a uniform movement in implied volatility across all tenors and strikes. |

4. Risk Management and Stress Testing

While real-world market regimes often exhibit asymmetric moves (Twists or Butterflies), the parallel shift remains the industry standard for:

- Scenario P&L: Rapid simulations to determine the trading book’s vulnerability to systemic shocks (e.g., +100/200 bps scenarios).

- Regulatory Compliance: A fundamental requirement within the FRTB (Fundamental Review of the Trading Book) and Basel III frameworks for calculating curvature risk and sensitivity-based methods.

- Hedging: Used as a benchmark for macro-hedging via linear instruments, such as Bond Futures or Interest Rate Swaps.

5. Parallel Shift vs. Vol-Slide

It is crucial to distinguish a parallel shift in volatility from a simple “slide” along the smile:

- Slide: A mechanical effect resulting from the movement of the underlying (the price moves to strikes with different IVs along a static smile).

- Parallel Shift: A genuine risk repricing where the entire surface shifts, reflecting a generalized increase in the risk premium (typically triggered by macro events or liquidity shocks).